Solving the Double Tax Trap with Strategic Insurance and Tax Integration.

The Client:

A Real Estate Entrepreneur with a Legacy at Stake

At 64, Mr. Gill had successfully grown a $20 million real estate corporation—Investco. He had already executed an estate freeze to cap the value of his preferred shares, believing this would secure a smooth transition of wealth. But as we discovered through in-depth planning, a significant problem remained hidden beneath the surface: a massive tax liability at death with no corresponding source of liquidity.

Worse yet, his will—though seemingly robust—wasn't aligned to support the post-mortem strategies required to minimize that liability.

The Challenge:

More Than Just a Tax Bill—A Liquidity Mismatch

A freeze had been completed, but that didn’t mean the estate’s tax exposure was resolved. In fact, quite the opposite. If Mr. Gill were to pass away with no further planning, his heirs would face:

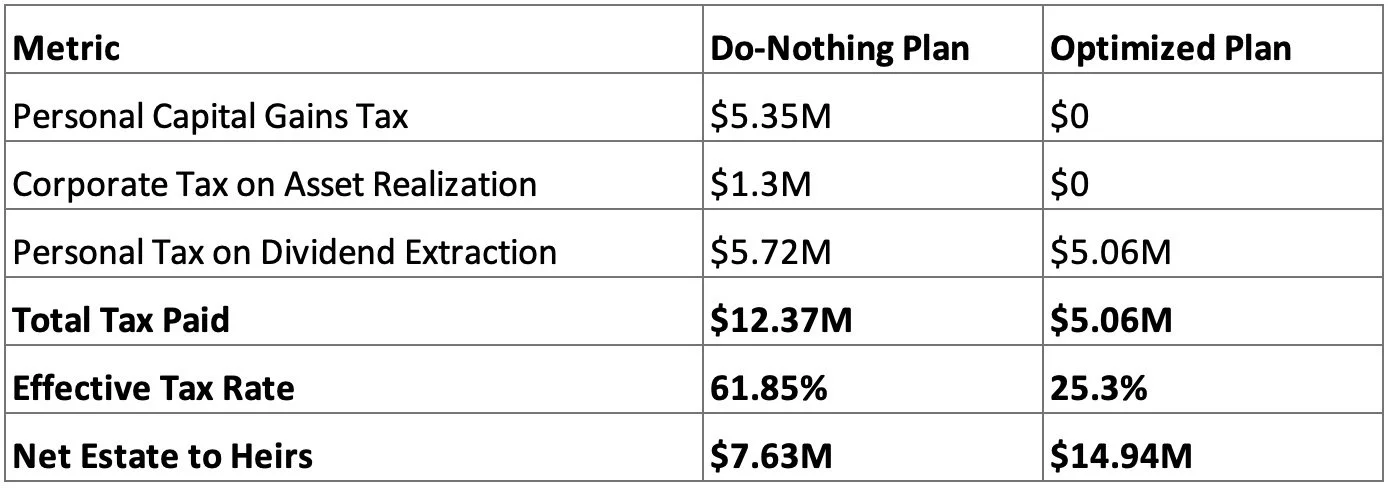

$5.35M in personal capital gains tax on deemed disposition

$1.3M in corporate tax on unrealized appreciation of corporate assets

$5.72M in dividend tax to extract remaining value from the company

That’s over $12.3 million in taxes—with no obvious pool of cash to pay it.

This is the classic liquidity mismatch: taxes are due, but the assets are tied up in long-term real estate holdings. Selling under pressure or borrowing at death are poor options. This is where insurance came in—not as a sales tool, but as a precision solution, modeled and sized according to the actual tax outcome we collaboratively designed.

The Strategy:

Collaboration Drives Strategy, Not Guesswork

Rather than default to a one-size-fits-all insurance recommendation, we did something different:

Pre-Death Modeling of Post-Mortem Planning

Together with Mr. Gill’s accountant and tax lawyer, we walked through post-mortem planning scenarios well in advance. We modeled the two key post-mortem strategies:A 164(6) loss carryback to eliminate the capital gain at death

A pipeline plan with an 88(1)(d) bump to extract corporate value with minimal tax

By projecting these strategies forward, we were able to estimate—with precision—what the after-tax estate value could be if they were properly executed. This informed our recommendation: a $2.65M participating whole life policy, corporately owned and funded over 7 years.

This wasn’t about “maximizing insurance”—it was about fitting the solution to the real tax and liquidity picture.

Legal Review: Aligning the Will with the Tax Plan

During our collaboration, the tax lawyer reviewed Mr. Gill’s existing will. It became clear that certain provisions might prevent the executor from fully accessing post-mortem planning tools like the 164(6) election or the pipeline transfer.

We worked as a team to:Identify provisions that could unintentionally limit tax planning flexibility

Propose and ultimately recommend a corporate will, to ensure the executor of Mr. Gill’s corporate assets could act swiftly and independently.

Confirm that the corporate structure and share classes would support the planned transactions post-mortem.

This legal alignment was as critical as the insurance or tax work—it ensured the entire plan was executable.

The Solution:

Insurance as a Liquidity Engine and Tax Accelerator

With the structure in place, the strategy unfolded in four parts:

Participating Whole Life Insurance

Funded with $202,800/year for 7 years, the policy created a $2.65M death benefit

Paid directly to Investco upon death

Boosted the Capital Dividend Account (CDA) by $2.65M

Created immediate liquidity to fund redemption, dividends, and taxes—precisely when needed most

Section 164(6) Loss Carryback

Estate redeemed ~$13M in preferred shares

Triggered a deemed dividend, then generated a capital loss

Carried loss back to eliminate the $5.35M capital gain at death

Capital gains tax: reduced to $0

The 50% Strategy: Balancing Taxable and Non-Taxable Flows

Only half the shares were redeemed upfront

Used 50% of the CDA and 50% as a taxable dividend

Preserved capital loss recognition (avoiding stop-loss denial)

Maintained dividend efficiency

Pipeline Strategy and 88(1)(d) Bump

Remaining shares transferred to Newco for a promissory note

Newco wound up Investco, executing the 88(1)(d) bump to real estate ACB

Investco’s assets were liquidated without corporate tax

Newco used proceeds to repay the estate tax-free

Side-by-Side:

With vs. Without Planning

The result? An $8 million improvement in legacy, thanks to thoughtful modeling, legal validation, and appropriately scaled insurance.

Key Takeaways:

Why Insurance Added Unique Value

Insurance Solves the Liquidity Mismatch

Real estate isn’t liquid. Taxes at death are. Without a predictable, tax-free source of cash, even the best post-mortem strategies fail to launch. Insurance provides timely liquidity, enabling those strategies to succeed.

Model Before You Insure

The right insurance amount isn’t guesswork. It’s the output of rigorous modeling. We don’t oversell—we custom-fit to the tax liabilities we help design.

The Will Must Match the Plan

Post-mortem strategies like 164(6) and pipeline require executor flexibility. A tax lawyer’s review and corporate will can prevent legal bottlenecks.

Three Professions, One Outcome

Insurance, tax, and legal professionals working as a unit produced a better estate result than any one party could have alone.

Could This Work for Your Client?

When insurance advisors work in isolation, clients are often over-insured, under-protected, or both. But when we lead with strategy—starting with tax modeling and estate structure—insurance becomes what it should be: a precise, high-leverage tool that enables the plan.

If your clients hold corporate assets and have done an estate freeze, they might think the hard work is done. In reality, it may have just begun. Let’s collaborate to help them complete the picture—and ensure their legacy stays intact.

This information has been prepared by Westmount Wealth Planning Inc. Westmount Wealth Planning is a subsidiary of Westmount Wealth Management Inc. Westmount Wealth Management Inc. is registered as a Portfolio Manager in British Columbia, Alberta, and Ontario.

This material is distributed for informational purposes only and is not intended to provide personalized legal, accounting, tax, or specific investment advice. Please speak to a Westmount Wealth Advisor regarding your unique situation.